US Private Debt Turmoil and its implications for Europe

23.03.2026|14 min

While the ongoing war in the Middle East has been a key concern for all investors, over the recent months a succession of events, essentially in the US, in the Private Debt segment of the market have raised concerns about its solidity.

Against that background, it is important to address the recent events in the context of the broad characteristics of the Private Debt market. It is key for European investors to understand the quite significant differences between the US and the European market, notably in terms of their institutional framework as well as their exposure to specific economic activities.

However, there is no room for complacency. The recent events should be taken seriously and investors should watch for signs of a potential broadening of problems, including a contagion to European markets.

Our assessment remains that in Europe, the Private Debt market should remain solid, barring an extremely high impact of the war on the ongoing economic expansion. Equally important, we continue to consider that our approach of extreme selectivity in our investments is a key factor in preserving value.

BDC’s woes

Investors have seen headlines of liquidity events around Blackstone ( BCRED), Blackrock (HPS), Apollo, Ares, Morgan Stanley-Cliffwater and Blue OWL Private Debt fund in the US. It is important to put these in the wider US context.

Firstly, the Semi liquid Private Debt funds in the US need to be put in the context of the overall Business development Corporations (BDCs) sector (150+ funds both public and private) in the US . These are tax advantaged investment vehicles for High-net-worth individuals (HNWI) and Retail investors that invest in private debt. The semi- liquid Private Debt market + BDC’s Asset under management (AUM) is estimated at around $500bln which some estimate to be around 30-50% of the managed Private Debt funds market in the US (around $1-1.5trln)

BDC’s and CLOs are considered a reasonable bellwether to US private credit as it is the first place to feel and observe the effects of mark to market (MTM), as they will show the latest estimated marks, defaults, restructuring and Pay-in-kind (PIK) provisioning, rating migration as well as well as leverage sensitivity.

Sentiment for BDC changed from a 2025 stance of “fundamentals still ok, earnings will normalize” to “valuation stress is now pricing a tougher credit and liquidity regime”

There are various causes for this sentiment change:

- BDC Valuations across both Public and private space have seen a general decline throughout 2025 with a significant dispersion of performance reflecting the start of credit quality fears.

- Fitch published in Q4 2025 default results which showed that defaults in lower Mid-Market (below $100 million) had increased to 9.2% and more specifically said that the below $25mln segment was the key driver to higher defaults in the US – Europe equivalent default rate is at 3.5-4.5%

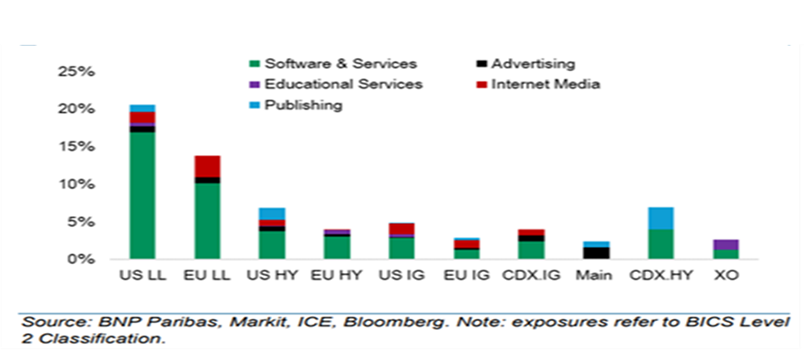

- Anthropic, an Artificial Intelligence company, released models believed to be able to handle numerous office solutions in many areas, leading to subsequent mark down the value of existing Software companies. This raised questions on the weighting of Software and tech sectors in portfolio’s – some BDC had high exposure (20%+)- and subsequent questioning of portfolio valuations

- The valuations and defaults concerns also led to some questioning the PIK exposure in portfolios as this could be just delaying a problem and kicking the can down the road

- Valuations have dropped from Mid 90’s to Low 80’s vs NAV which also led some to fear some forced selling due to Margin calls on leveraged positions or to meet liquidity needs

- Lower coupons given rate cut scenarios expected during 2026, although this may change.

BDC’s: valuations have been declining since late 2025

The US are by far more exposed to AI and AI disruptions than Europe

Investors’ reaction and liquidity concerns

The concerns and uncertainties affecting BDCs have already led to average redemptions within the BDC market rising in late Q4 2025 -Q1 2026 from 1.6% to 4.5% of NAV for Private BDC’s.

Clearly the requests seen in the headlines were more in the 7-14% range. Blue Owl has several retail vehicles which also saw redemptions requests. The gates for Private BDCs are well documented and therefore of no surprise. Most gates are set at 5% and some can be increased by another 2% at the discretion of the BDC.

There has been a mixed response by Managers to the redemption requests. Some have met the redemption requests despite being above the gates, others have used their discretion to raise the gates by 2% and one or two have had to suspend the gates for the moment. This has led to further liquidity fear by BDC investor and the 1Q 2026 redemption rate remains hight around 8-12%. Accordingly, in the short term this topic is not going away. It would also seem that Cliffwater and Blue Owl (as reported in the press) have raised $2.5bln through secondary sales of Private credit. There is further fear that if this liquidity withdrawal continues it could start to hit then revenues of the most impacted General partners (GPs). At Blackstone and Blue Owl, private credit retail funds account for 13% and 21% of fee revenue respectively.

What are the current concerns by Retail and Institutional LPs for US Private Credit?

- Borrower credit deterioration in below $100 million EBITDA companies – AI exposure, leveraged balance sheets, few or no covenants, more restructuring with higher PIK exposure leading to potential hidden problems

- Keeping an eye on non-accrual rates at BDC’s, realized loss rates, watch list share, and interest coverage trends

- Fund leverage and refinancing risks

- Valuation lags/ Stale marks

- Interconnectedness’ with Banks and insurers – warehouse line availability, NAV loan usage, bank-transfer links, insurer demand for private credit and tightening in bank financing terms to the sector

- While gates are working as documented, they can lead to further contagion

Many of these concerns seem to point to a fear of a generalized weakness in the underlying assets of BDC’s. However, portfolio metrics form BDCs do not seem to indicate such pattern, although clearly there are pockets of weakness.

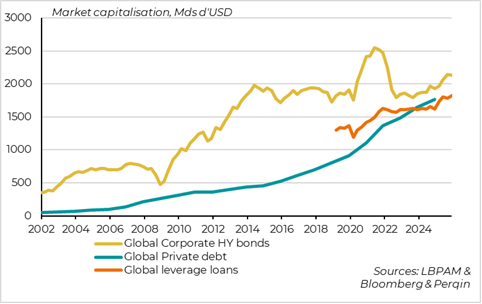

A late cycle bifurcation among managers as Private Debt has quadrupled in 10 years

In fact, in our view, even putting aside some specific shocks, such as the AI, some of the weakness we are witnessing among some players seem to reflect a late cycle bifurcation in the asset class. Indeed, the Private Debt market has almost quadruple over the last 10 years. Accordingly, it could be natural to see managers performance dispersion to begin to show. This become evident through watch lists, % of PIK assets, Covenant resets (both can be positive as well as negative).

We believe that good managers with disciplined First lien books, showing proven resilient performance will win out in this cycle.

It is also important to highlight that the concerns related to the interlink between US Private Debt actors and Banks could be seen as a potential systemic risk. Indeed, too high exposure of banks to the sector in case of broad defaults could lead to paralysis in the financial system. At this stage, despite some opacity, regulators do not see such risk.

The European market appears much more resilient

Thus far we have not witnessed in continental Europe the type of event seen across the Atlantic. However, questions might arise concerning the quality of the debt assets in Europe as well as about the quality of the asset managers or liquidity fears. This could be seen as a natural spillover of the issues seen in the US.

However, at this stage, the spillover effect to Europe will be more psychological than trend following in liquidity requests. There are several reasons for this:

- Retail has less exposure to the asset class in Europe but that is growing.

- Retail Vehicles in Europe are still in their infancy vs US and penetration to retail is much lower

- European companies below $100 million EBITDA are more resilient – less leveraged, loans are well covenanted, there are better cash buffers and more potential for internal growth opportunities in creating national or Pan European champions

- Defaults are lower and recoveries slightly better, however there is still an expectation that defaults may rise but at a slower rate in the US.

- Insurance companies in Europe have very little leveraged exposure to the asset class, so less potential valuation volatility or potential need for secondary market access.

- Exposure to AI is lower than in the US

The US are by far more exposed to AI and AI disruptions than Europe

The retail penetration of private credit in Europe vs US is still in its infancy, so any liquidity contagion will be limited. From a credit cycle standpoint there is still a relative value in Europe vs US.

The sub $25 million EBITDA GPs are predicted to see rising defaults, more pressure on liquidity and higher leverage sensitivity while European sub 25 million EBITDA -Direct Lending will still be under pressure but generally are better protected structurally, with lower leverage and more resilient credit setup. Europe looks the more disciplined on leverage and creditor protection.

Conclusion

Understandingly, the succession of bad news stemming from the Private Debt market in the US has created a lot of anxiety. As we explained, many of the asset-value issues as well as the liquidity stress associated to the request for redemptions has been concentrated in BDCs, affecting some large names, such as Blackrock, Apollo, Ares or Blue Owl. However, at this stage, the evidence does not point to a generalized deterioration of the Private Debt assets owned by the large players. Also, despite the interlinkage of Private Debt managers and Banks, the fear of an imminent systemic risk seems exaggerated.

At the same time, after a very rapid growth in the asset class assets, it seems that we are witnessing a late cycle bifurcation, with weak players likely to be hardly hit.

The issues that have arisen in the US have not touched continental Europe. Despite the fear that some contagion coming from the US could affect the asset class, we believe that there are many differences that make the European market more resilient. Barring a very negative economic impact of the ongoing war, we believe that the European market should remain solid.

We will continue to monitor very closely all the dynamics in the market on both sides of the Atlantic. But, more importantly, we will continue to focus on our very selective approach in the Private Debt segment aimed at preserving value over the long run.